Despite religiously tracking my net worth, the main metric I tend to focus on when evaluating my portfolio is the income that it generates. After all it is the portfolio income that will one day pay my bills and keep me in Werther Originals.

Monevator has written an excellent article on targeting your current monthly income as the number you need your portfolio to generate if you want to become truly financially independent and retire early. This article articulates perfectly the reasons why I focus on income generation as opposed to capital gain as part of my approach to investing.

However there is no escaping the fact that once you know how much you need your portfolio to produce every month, you then need to work out how much capital you will need in order to generate that income.

Of course the amount of capital required will depend entirely on the yield of your portfolio. The easiest way to work this out (and the method I use) is to use your portfolios historical yield.

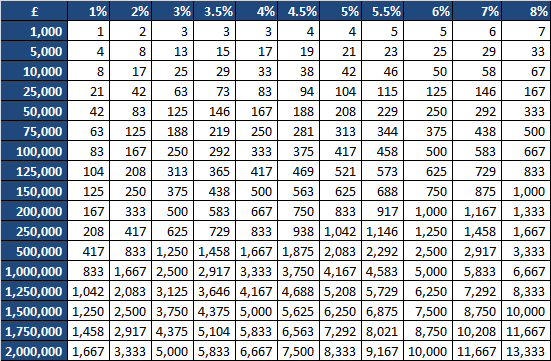

The chart below is very useful for giving you a rough idea of how much you need to invest in order to achieve a set monthly income.

Fig 1. Monthly Income Chart

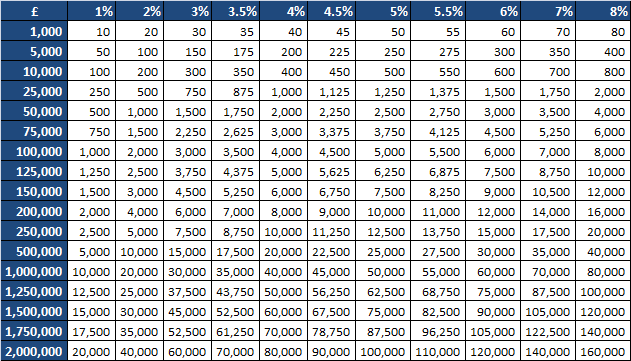

If you prefer working with annual figures then here’s the same information but with an annual view:

Fig 2. Annual Income Chart

You can use the above charts in two ways:

1. Check how much your current portfolio yields per month. Simply look up your portfolio size on the left hand column then read across to the column that’s header equates to the yield your portfolio generates. For example if you’ve got £50,000 invested in your ISA and it yields on average 5% then your currently generating income of approximately £208 per month in income.

2. Estimate your target portfolio size based on your required income. First decide on your desired monthly income. Then find the number on the grid that is closest in the column whose column header most closely matches your portfolios yield. Look across for the left hand column and you now know how big your portfolio needs to be. For example lets say my portfolio yields 5% and I require an income of £2,000 to cover my expenses. I’d need a portfolio of £500,000 in size to return £2,083 per month.

Hold on though…what about tax?

Of course the above tables show income received as pre tax. If all of your portfolio is squirrelled away in an ISA/NISA then no problemo. If however your investments are subject to tax you’ll need to factor in the income tax you’ll pay into the equation.

When I get stressed at work I close my eyes and remember that being there is enabling me to move downwards in these tables.

Think In Expense Replacement Terms

Being naturally risk adverse my main driver to become financial independent is to be able to cover my living expenses from the income my portfolio sheds off. Once I achieve that then I’ll also want to ensure that the portfolio can also keep up with inflation and if possible maintain a small amount of real term growth too.

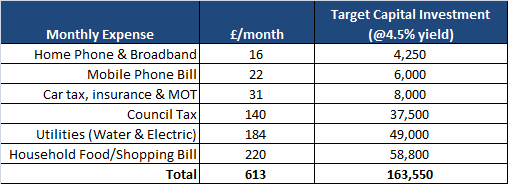

Lets just worry about paying my expenses for now. Lets consider an example of how much I’d need in my portfolio to cover some of my main monthly expenses (assuming a 4.5% yield).

Based on the above chart I need to amass £163,550 before the average monthly income my ISA produces covers these expenses. In fact I wouldn’t even need £163k. Until the point when I started drawing the income the portfolio produces, the dividends received will be compounding up meaning that in reality I would need less than the £163k.

ISAs/NISAs are very attractive vehicles for a mid 30s chap like me to be saving into. There’s a purity about them in that any gains are free from tax. I find glancing at the tables above from time to time keeps me motivated to keep saving, keep investing and make the most of any capital I can acquire during this period of my life.

Leave a Reply to Hariseldon Cancel reply