I’ve been debating over the last few weeks about how much contribution to make to my personal pension. As with most of the unlucky under 40’s in this country, I’m on a defined contribution pension scheme. Up until now i’ve not made any contributions of my own, instead i’ve been focusing on diverting my cash into building future income streams that I can draw on before I reach retirement age. To date all spare income has been invested in my property portfolio and stocks and shares ISAs. The plan has alway been to retire early and up until now my pension has had to be on hold to try and make this happen.

Recently I’ve been thinking more and more about the tax benefits to be gained from making additional pension contributions and doing a few sums. Whilst reading through the HMRC website I stumbled across this nasty little paragraph:

If your ‘adjusted net income’ – read more below – is over £100,000, your Personal Allowance is reduced by half of the amount – £1 for every £2 – you have over that limit. If your income is large enough, your Personal Allowance will be reduced to nil.

So for every £2 you earn over £100,000 your personal tax allowance is reduced by £1. In effect this means that if you earn over £100,000 per year, any income between £100,000 and £120,000 is effectively taxed at a rate of 60%.

While I realise I’m in a fortunate position to worry about such things, this is exactly the kind of inconsistency that makes a lot of people hate our income tax system. Personally I believe either a pure flat rate tax rate or a much more gradual tax scale would be much more transparent, fairer and easier for all to understand for all.

Play The Game

Without a simple tax regime in place in this country, the likes of me (and probably you) are incentivised to find ways to optimise our tax affairs in order to pay as little tax as the regulations allow, in order to get the most from the hard earned dosh we get paid.

There’s often a fine moral and legal lines between tax avoidance (the legal tax game) and tax evasion (go to jail stuff). What is unfair is that it is usually those on lower incomes that don’t have the means, inclination or education to pay the tax game.

Lets look at the example below…

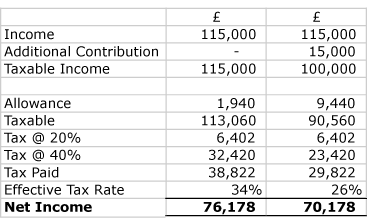

Assuming you get paid £115,000 your tax free allowance gets reduced down from £9,440 to 1,940 by the fact that you earned £15,000 over the £100,000 threshold. Overall you’re effective tax rate is 34%. However if you make an additional pension contribution (as shown in the third column) of £15,000 two things happen.

- You gain back your full tax free allowance of £9,440 because your taxable salary is £100,000.

- You will receive a 20% tax benefit that your pension company claims back from the government. This means they’ll add on another 20% to the £15,000 meaning your pension actually benefits by £18,000 not just the £15,000 you put in.

Of course don’t forget that if you make a pension contribution out of your net salary and are a higher rate tax payer you’ll need to claim back the extra 20% via your self assessment form.

Leave a Reply