With all the talk in the media of deficits, lack of growth, negative rates and deflation you’d be forgiven for thinking that the stock market ought to be in the doldrums. But what’s this flashing up on my screen…

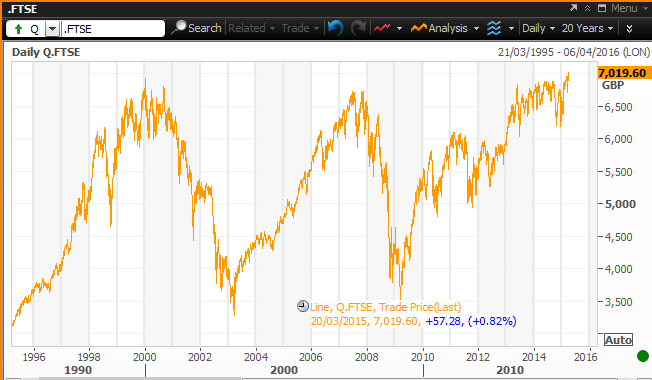

The FTSE just hit a new record high, breaking the 7,000 mark for the first time ever. As you can see below it came awfully close to the 7,000 mark back in 2000 and again in 2007.

Government bonds, once the bastion of safe yield just don’t cut the mustard any more. Last week 7 year German Bunds turned negative meaning that you now have to pay the German government for the privilege of lending them your money for the next 7 years.

The world had it’s fill of CDOs, CLOs, CDO2, ABX, CDXs and MBSs back in the first half of the 2000’s and that didn’t really turn out too well. While some of these derivatives still trade the world likes it’s income much more vanilla these days.

Banks are de-leveraging, governments are making (mainly feeble) attempts to de-leverage, hell I’m even de-leveraging myself despite record low interest rates. In these uncertain times investment in big, expensive long term infrastructure projects just isn’t what most investors want to do with their money.

So looking around there’s not many places to head for income apart from property and developed market stocks. Markets have been pumped up by the QE money that is sloshing it’s way around the system looking for a home and some sort of income.

So What Next?

Well if you look at the chart above again a reasonable assumption might be a crash back down to the 3,500 level like the last two times. How might that happen? Well there’s many way to skin a [fat] cat but…

- Increase in interest rates (inevitable at some point) sparks property crash

- Property crash sparks stock market crash

- Throw in some Grexit/Putinism/Other Surprise Badness to really get the sell of going

Of course I have no idea what will actually happen to the markets over the next year. Based on my lack of fortune telling ability I’ll keep calm and carry on my balanced approach of de-leveraging my property investments, investing in defensive income producing shares/etfs and reducing income tax via pension AVC’s.

See you on the other side!

Of course if you correct that chart to allow for the devaluation of it’s unit of measure (£’s) through inflation we’re still nowhere near a new high. That honour still goes to the year 2000.

RIT,

Yes, the chart doesn’t take in to account inflation or dividends paid out. I find it strange that the technical analysts place so much emphasis on these type of ‘break throughs’.

Such are the weaknesses of the human mind! Not being Vulcan-esque we still let illogical things direct how we operate and think. What is more worrying, however, is that many of us still think we are more Spock-like than we are!

It’s nice when things like this emerge as it reminds us of this fact: we are not entirely logical. With but a little thought we realise 7,000 today is miles below the value it was when it reached the value several times. Yet still we see it as a critical (and positive) landmark.

Of course, it is good news in some regards. But not as important as it often comes across!

It is interesting to see that the only returns from UK stocks for the past 15 years came in the form of dividends. Is there a resource that shows historical FTSE 100 dividends for the past say 50 years?

I think that the next 20 years will be different than the past. Hence that 7000 level will likely seem like it was in retrospect a nice entry point to scoop up the best and brightest UK blue chip stocks if/when we meet up for a few beers in 2035 🙂 And I would bet that an investment today, while spending dividends each year will likely pay 14 – 15% on cost at that time too

DGI,

I like your optimism and I definitely hope you’re right!

Hi UTMT,

The key difference, and why it’s very unlikely we’ll “ever” see 3,500 again, is the dividend.

In 2000 at 7,000 the yield was about 2.1%, so a crash to 3,500 would double the yield to 4.2%, which historically is only slightly high.

In 2008 at 7,000 the yield was about 3.1%, so the crash to 3,500 took it to 6.2%, or thereabouts. That’s a very high yield which was the main reason (in my opinion) why the market rebounded so quickly (that and the fact that the world didn’t end).

In 2015 at 7,000 the yield is 3.4%, so a crash to 3,500 would take the yield to 6.8%, which is way above average.

Of course we could get to 3,500 but we’d need a massive crisis to do it, so I think 10,000 is more likely than 3,500 from a valuation point of view.

UK Value Investor,

Buying at 3,500 with a yield @ 6.8% would be an exciting prospect but as you say, unlikely to happen without a seriously big crisis. It just goes to show how entirely unpredictable the financial markets are trying to predict these peaks/troughs is an activity that is pretty much impossible.

So if we did get a crash… where might it go down to? 4,500 a lot more likely that 3,500… but as John says, I feel like 10k is more achievable and likely over the next few years… unless we get a crazy Putinesque/other situation to whack the market on the head. Anyway, I am always up for buying more great dividend stocks.

Cheers

“…you now have to pay the German government for the privilege of lending them your money for the next 7 years.” Wow, I think I somehow missed that headline that last couple of days. Bond rates for the Germans that bad huh? I guess some investors are prepping their money for the anticipated rise in the US bonds by the end of this year.

Mark Yenter,

There are several different reasons why investors might do something so seeminglt illogical as pay someone to lend them money. Of the top of my head here are some possibilities:

– Expectation that the ECBs QE bond buying program will cause prices to increase

– A negative yielding bond can still produce a ‘positive’ gain if you’re in a deflationary scenario

– There’s not that many ‘safe’ places to park money these days, some are willing to pay for the safety of the German government

– Many bond funds are obliged to hold German Bunds no matter what the current yield is

– A play on currency appreciation

– Betting that prices will rise further

UTMT,

It is a strange thing. When I saw the FTSE had “smashed” through 7,000 last week I found myself quite happy about it. But it’s a psychological barrier and not really that different to 6,950 or 7,050. It gives some weight to the idea that investors are definitely not rational.

I too am struggling with the idea of putting any money into bonds at the moment, surely prices will only go down from here? Although there was an article the other day suggesting that a drop in base rates is know as likely as an increase. Nothing like speculation to keep you on your toes 🙂

Mr Z

MrZombie,

We’re very much in uncharted territory in the bond market at the minute with so much of the government bonds slipping further into negative yields. Also from what I see the liquidity in corporate bonds is continuing to dry up significantly which doesn’t bode well for the credit markets.

Love the fact that it pretty much dived straight back down below again… People attempting to predict another crash maybe? 🙂

Agree with comments above though that we *should* never see the likes of 3,500 again. I wonder when it will hit 8000… 2 years time? 1 year?! Who knows!