Being relatively young (mid thirties) means that NISAs (ISAs) are the savings/investment vehicle of choice for me when it comes to the stock market. While there are generous tax breaks on offer when you put money into a pension I currently prefer NISAs for the following two reasons:

- Any future income or capital gains generated are free of tax

- Unlike a pension I have instant access to my capital and/or income if required

Tax is a shit. Assuming I live to 90 years old then I’ve potentially got 55 years of income tax to pay ahead of me. Eeek!

The prospect any investment income I receive being free of tax for the next 55 years is a much more interesting prospect than lining the chancellors pockets for the next half century. This is the reason why I’m stuffing my ISAs with gusto and leaving the additional pension contributions until nearer the time when I can get my hands on my pension savings.

Measure Your Progress

A while ago we posted some income tables that allow you to quickly look up how much capital you’d need invested in a tax free vehicle like an ISA in order to achieve a given monthly or annual income. I find myself continually going back to these tables to gauge the progress of my NISA accounts.

I’m fascinated with measuring the trailing 12 month average income my portfolio produces. This is the one number that means the most to me and motivates me to save and invest more, more so than my net worth. The fact that NISA income is tax free makes it even more delicious!

As I see this number increase each year I sense my financial freedom coming closer. This is the number that (in conjunction with my monthly expenses) will ultimately have a big say in determining when I reach financial independence.

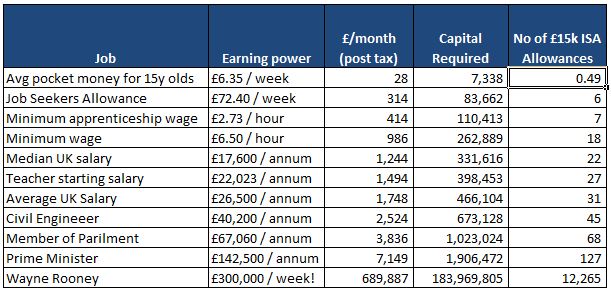

While the number is only relevant when added to my other investment income and compared to my monthly expenses, it is interesting to see how it compares to common income figures that get banded about.

Below is a table of a variety of jobs. I was interested to see how much NISA capital you would need in your war chest in order to generate the equivalent income. In the examples below I’ve assumed the ‘capital required’ is producing an annual income yield of 4.5%.

Upon first glance it might seem quite daunting that you have to save the equivalent of 31 NISA allowances in order to produce a tax free income equal to the take home pay of the average UK salary (£1,748 per month). It’s no lie that filling ISAs for 31 years to achieve the average UK wage doesn’t sound like a fast track way to financial independence.

However remember that there are a few other factors that can/should be working in your favour:

1. Ever increasing capital. Until you start drawing you’re income you’d be well advised to follow rule #1 of the dividend investing rules. By compounding your income early on you can seriously reduce the amount of capital you’ll need to inject into your income machine.

2. 4.5%. If you can return more than 4.5% per year in returns (capital + income) then you’re capital pile will increase much faster. Of course if you’re willing to take on more risk then you’re might be able to return significantly more than 4.5% – buyer beware though!

3. Join it up. If you’re married both individuals get a separate NISA allowance. This means that a married couple can stash £30,000 per year into NISAs, halving the time it takes to reach the desired income. The only tricky part i finding £30,000 of disposable income to stash away each year.

4. Steady old boy. Don’t forget that at some point in the future you’ll likely receive some sort of pension income, hopefully both in the form of a state pension and a personal company pension or SIPP. This means that at some point in your retirement your income will rise. This means that you’ll need less NISA income to maintain the same disposable income as before you started receiving your pension. This means you may want to draw down some of your capital in the period before you start drawing your pension/s.

5. Screw that. Of course the less you spend the less income you’ll need. No matter how you do it saving money is just as, if not even more powerful than increasing your investment income!

Hello,

tax is a shit.

I like the table, it’s good to be able to relate your savings back to something real. Especially in terms of income. I’m somewhere between pocket money and job seekers allowance. Haha. Nice.

I have only just come to a similar decision re ISA vs pension, but have been saving into a pension for the last few years. D’Oh.

Mr Zombie,

The important thing is that your journey to the bottom of the table has started 😉

Saving into a pension is not the worst thing in the world. What scares me is that your money is locked away and the government have control of when you’re allowed access to it. I predict they’ll be a good few different governments making stupid decisions before I’m able to get at mine.

Yeah that’s true. Starting it off is one of the hard parts.

Yeah, there is a huge regulation risk with your pension. Don’t want to rely on just the one vehicle. Or even provider. Still. The employer contribution is hard to ignore!

To be honest I think I will diversify my NISA providers once they get to some critical mass, it’s good to be paranoid 🙂

Have a good weekend

I’m also between pocket money and Job seekers allowance! Got to start somewhere though ay. We are also already “diversified” over 3 different ISA providers because I didn’t read Monevators cheapest UK brokers table before opening the first, and then didn’t read it properly after opening the second… haha. Third time lucky with CSD (I think)!

Great idea for a table and article UTMT, love it.

In a way it makes the task of FI seem even harder when you look at the average income but your 5 subsequent points rationalise the figures back down to something that seems achievable again. Cheers!

FIREstarter,

Diversifying your ISA holdings over a number of providers is no bad thing, particularly as your portfolio grows over time. Of course minimizing any fees you’re paying should also be a priority 😉

Glad you like the table. I think it puts into perspective how hard FI is to reach ‘outright’. Of course when you consider that most will opt for a new career or freelance/part time work (so will still have some wage income coming in) it’s not necessarily so tough to attain.

Hi UTMT

Great post! It’s funny how when I first started saving towards FI, I was chucking everything at my SIPP, until, I realised that I would still be taxed on it. So, I tend to split my investments now between the two, though am likely to build my NISA up more.

A most interesting table too – it currently looks like on average, I spend just over what someone on minimum wage receives post tax, although my earning power sits somewhere between the Average UK Salary and a Civil Engineer.

The annual FI salary I’ve used for my own calculations is £20k, which should provide me with more than enough. As you say, my own savings/investments will be bumped up by my company pension and what’s left of the state pension!

Hi Weenie,

It sounds like you’re spending is well outweighed by your current earning so your journey to FI should be making great progress!

Don’t forget as well that you’ll most likely have paid off your mortgage, and also won’t have the cost of going to work i.e lunch, transport etc, so the amount that you’ll be able to get by on can be much less than you’re current take home pay, which also helps make the FI target easier to obtain .

Steve,

Great points. It’s a fear most people have that their spending will increase when they ‘retire’ when in fact most people I have spoken to have said their spending fell significantly.

I think the one areas where SIPPS have a tax advantage over ISAS is if you pay higher rate tax now, but expect to pay only basic rate tax in retirement.

Then you can get higher rate tax relief on the SIPP now and pay basic rate tax after retirement.

If you expect to be on the same marginal rate now and in retirement, SIPPs have no tax advantage over ISAS, so in that case you might as well take the flexibility of the ISA first.

Hi Jeff, that’s where I am – I’m not in the higher tax bracket and unlikely to be so soon unless I unexpectedly have a bit pay hike! More into my ISA!

The other thing that can swing it for a sipp over an isa is where you get a matched contribution or employers ni rebate on the salary sacrifice.

THe Rhino,

You’re spot on. If your employer offers matched contributions or NI rebate then it is almost a no brainer to turn those down. While my employers defined contributions are quite generous, unfortunately they don’t offer any additional matching or NI rebate 🙁

Interesting to read your conclusion about the SIPP vs ISA decision. Due to spending all my surplus income renovating a rental house a few months ago I’ll have very little spare cash for my SIPP contribution this tax year. That means deciding whether or not to transfer a significant amount from an ISA into my SIPP before 5th April. As a current higher rate tax payer expecting to pay a lower rate of tax in retirement it should be a no brainer for me, but like you I’m cautious. Pensioners are currently treated very favourably because there are so many of them and they tend to vote. Fast forward 20 years or so and things could be very different (online voting and lots more baby boomers born in the 2010s than middle aged generation X’ers like me) but nobody can predict whether wealthy SIPP-holders or ISA millionaires will be targeted. Or if income tax and national insurance will be merged, resulting in higher tax rates for the retired generally.

Simply running the numbers tells me that every £1,000 of higher rate tax I eliminate by transferring £1,000 of ISA will be turned into £1,250 in the SIPP and will also give me a tax rebate of a further £250 in cash which I can put back into next year’s ISA allowance. Using the 4.5% capital/income rate in your article, that means I’d be converting a £45 tax free income into £56.25 that’s subject to tax plus £11.25 that’s tax free. If I end up paying tax at 20% on the SIPP element then my net income will still be £45+£11.25=£56.25 so 25% higher than if I leave everything in the ISA. In fact I’d have to find myself paying 40% in retirement before the result was equalised. And that’s without considering the possibility of withdrawing a tax free lump sum from my pension pot, if that concession remains.

So it really comes down to deciding whether the flexibility is worth the cost. Perhaps the best thing is to try and keep the balances in each type of tax shelter roughly equal to spread the risk. On that basis it might be sensible to keep using the higher rate tax relief while it’s still available and pay into my SIPP, because I might not keep earning over the threshold as I get older, or a future government might decide to reduce the available tax relief anyway.

BeatTheSeasons,

Thanks for the calculations, very interesting. I like the idea of using the 20% cash rebate from a personal pension contribution to stuff into an ISA.

I make additional pension contributions from time to time as well as stuffing the NISAs. As with most things financial I find a balanced approach best in order to minimize/dilute and risks. There is certainly no one size fits all approach for the NISA/Pension contributions as the comments above show, particularly when there decades of political interference ahead that can potentially change the rules significantly.

A SIPP really makes most sense if you are lucky enough to earn 100 – 120k where you would get 60% tax saving due to regaining the personal allowance on top of higher rate tax relief.

Marco,

Great point. That 100-120k 60% tax rate is something i’ve written about previously. It’s the perfect example of a terribly designed tax system!

Great post. Good idea to put lump sum returns into a real life context. It makes you remember the value of an earned income (until passive income catches up that is)!

My view on pensions mentioned in the comments above uses the well used snowball analogy. Given the main benefits of compounding coming in the later stages of investment, it makes sense to have a bigger snowball at the start so utilising the tax relief (and any extra an employer wants to match) earlier in a pension is more valuable than an ISA to generate returns, up until the point where the pot will be big enough (given estimated returns) to hit the first income tax threshold on your chosen source of retirement income! Then it becomes a bit more complicated… Thats all provided you arent touching either until you hit you’re FI target.

Sean,

You make a great point that getting that (pension) snowball bigger earlier will potentially make a big difference in 20, 30, 40 years time. The issue I have is that I’m aiming to ‘retire’ about 15 years before I can get my hands on any pension savings. This incentives me to maximnise my NISA savings while I can. The reality is that a balanced approach is probably best (unless you’re close to retirement).

I agree a balanced approach is best. Considering investment capital and timescales is important though. E.g. if the “capital required” numbers keep up with inflation (no investment returns), just by withdrawing a 15th of this sum each year until you retire, you’d have much more than the 4.5% income figures.

Your pensions could then pick up the slack…

I too, intend to “retire” 12 years before i can get hold of a pension and 24 years before i get the state pension and other pensions (without penalty). The more pension compounding in the background early, having been topped up by employer / tax man, the closer to £0 my ISA can be by the time i get there. I want my pension to be an income replacement / top up, not just surplus cash because my ISA yield is “enough”.

The biggest impacts on my ISA will be the amount i can invest through increased earning / reduced spending, not my returns. This is neatly demonstrated by the “capital required” figures in your article if you use short (<10 years) investing timescales to reach each one.

I havent seen capital reduction discussed often on blogs, but its built into my plan. I think FI numbers are pretty conservative already as they usually assume you dont get any income, other than passive. Not even finding a penny on the floor, let alone a penny of earned income!